NVDA's Spectacular Surge: Unveiling the Roaring 20s in Tech

Markets.com | Feb 22, 2024 09:56

- US futures jump after Nvidia’s bumper earnings; NVDA +13% pre-mkt!

- European indices rally, Stoxx 600, DAX fresh highs – London still looks on forlornly

- Nikkei beats 1989 closing high – the escape from deflation is here

Is This the Roaring 20s?

NVIDIA (NASDAQ:NVDA) whipsawed in after-hours trading as investors digested startlingly good results, before deciding that they really were as good as they looked to send the shares up 9% after the bell after initially dipping by 6% - now trading +13% in the pre-mkt trade! The company declared the AI ‘tipping point’ as revenues surged by a remarkable 265% over last year, and up 22% in the prior quarter. The company posted $22.1bn in revenue vs the forecast $20.55bn and $4.93 in earnings per share, against fc $4.64. Data Center sales – which now make up the bulk of the business - were up 409% to $18.40 billion, with over half going to large cloud providers.

I don’t think there is much to fault. “Fundamentally, the conditions are excellent for continued growth” in 2025 and beyond, CEO Jensen Huang said. The one blot on the copybook was China, not that anyone seems to care. "Data Center sales to China declined significantly in the fourth quarter due to US government licensing requirements,” the company said, with Huang noting that "this last quarter, our business significantly declined as we paused in the marketplace, we stopped shipping in the marketplace. We expect this quarter to be about the same. But after that, hopefully, we can go compete for our business."

All that matters is the massive structural shift.

“Demand is surging worldwide across companies, industries, and nations,” said Huang. “The year ahead will bring major new product cycles with exceptional innovations to help propel our industry forward."

The positive report sent shares in AI and semis higher – ARM jumped 8% after-hours, AMD (NASDAQ:AMD), ASML, and Infineon +4% and Supermicro +13%.

European shares firmed nicely, led by the DAX’s 1.5% gain to a new high led by autos, with the Stoxx 600 hitting a fresh intra-day record high even as Nestle fell 4% to weigh on the food and beverage sector. The FTSE 100 was more languid, up a modest 0.1% and still tracking below the 7,700 resistance area. It’s also helped drive the Nikkei 225 to a new all-time high as Asian tech shares were buoyed by the results. Everyone’s gone Japanese it seems - corporate profits booming, yen weak, chipmaking equipment makers seeing huge demand, reforms by the Tokyo Stock Exchange that have led companies to increase shareholder returns big shift nationally away from saving to investing - new capitalism drive, signs of emerging from deflationary cycle to inflationary trend not quite the froth of 1989. Meanwhile, Chinese shares continued their recovery.

Earlier Wall Street had edged up a bit for the session, though the Nasdaq slipped a touch as Nvidia led a broad decline for tech ahead of its earnings, which had seen huge anticipation and wild expectations for volatility in the stock – as indeed it turned out. Needless to say, the Nvidia effect has sent futures soaring with SPX looking to open at a fresh all-time high.

Lots of earnings this morning. Lloyds (LON:LLOY) shares fell as it set aside £450m to cover a car finance probe by the FCA. It’s maybe less than the market feared but the outcome of the investigation is still unknown. There is maybe a worry about how Lloyds has come up with the £450m figure – worst case scenario is said to be in the billions so perhaps some skepticism and sense that this number will have to rise materially. Full-year profits at the bank though rose to £7.8bn, thanks to higher interest rates. Net interest margin guided at 290bps which is in line with forecasts, and buyback also in line at £2bn, the same as last year.

Rolls-Royce (LON:RR) shares surged 8% higher as it beat profit forecasts for the year. Underlying profit of £1.6bn for 2023 was ahead of the £1.4bn expected and guided, whilst it also said profits would rise 6% this year, which was ahead of forecasts. In Germany, Mercedes rose over 4% as it topped Q4 sales forecasts and upped shareholder returns. Beazley led the FTSE 100 gainers with a ~9% rally on a guidance upgrade and plans to hand shareholders $300mn after its undiscounted combined ratio – a measure of underwriting performance improved from the “low-80s to mid-70s”.

FOMC meeting minutes – this down-the-running order shows how big the Nvidia/AI story is becoming – showed:

"Most participants noted the risks of moving too quickly to ease the stance of policy" and that rate cuts wouldn't be "appropriate until they had gained greater confidence that inflation was moving sustainably toward 2%".

Meanwhile, the Leading Economic Index from the Conference Board is now down by 13.4% from its recent all-time high, this decline is only ever usually seen during a recession, underlining what an odd cycle this is.

Germany comes to terms with its economic problems - slashes its growth outlook – 2024 GDP seen at +0.2% from a previous estimate of +1.3%. And this morning it’s clearly not great news – flash manufacturing PMI for Germany slipping to 42.3 from 45.5, and well below the expected 46.0. The flash manufacturing PMI for the Eurozone declined to 46.1 vs 46.6 previous and an expected improvement to 47.0. Services climbed to the breakeven 50.0. France’s report was a little healthier than Germany’s, but the picture is still pretty uninspiring. The PMIs seem to have cooled the somewhat overheating rally in the euro overnight, with the breach through the 200-day running into resistance at the 50-day.

And finally, the Chancellor is said to be considering 99% mortgages – what could possibly go wrong?

FX

Overall, the strong risk trade seems to be weighing on USD, which has slumped in the last 24 hours or so on improved attitudes to riskier bets despite the 10-year holding firm at 4.3%. EUR/USD and AUD/USD have both pushed up through their 200-day SMAs, whilst cable has extended its breakout to move clear of the 50-day SMA.

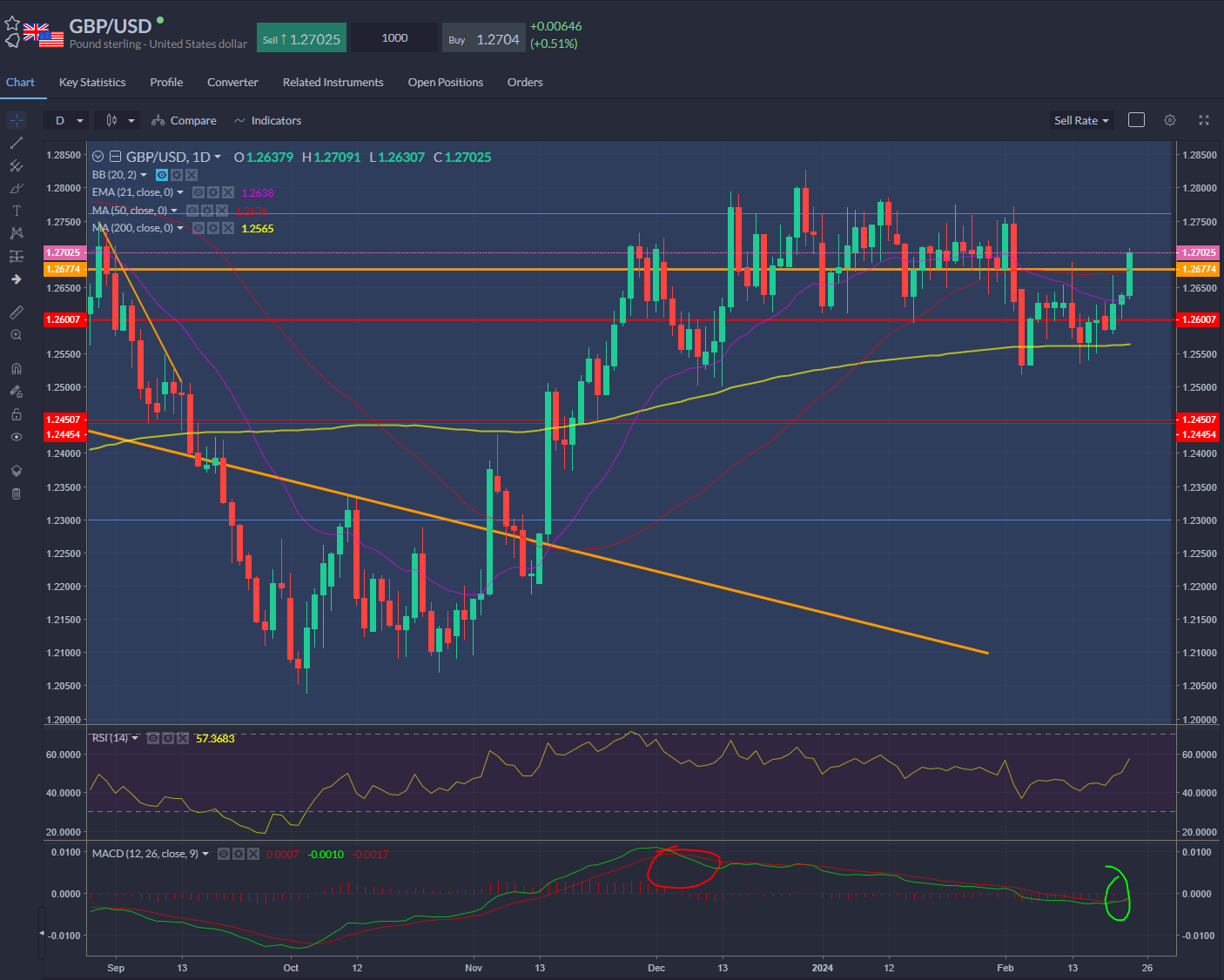

GBP/USD – that MACD move from below the baseline I mentioned yesterday has been confirmed – solid rally with risk bid, bulls look to chunky horizontal resistance around the 1.2750/1.280 area.

EUR/USD Daily – See the SMA Envelope

EUR/USD Hourly – See the Hot Rally Overnight Coming Up Against Those Weak PMIs

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.