2 Beaten-Down Tech Stocks to Buy in 2023

Investing.com | Jan 04, 2023 12:57

- Wall Street started 2023 on a sour note

- Concerns such as rising interest rates, high inflation, and a slowing economy will continue to impact sentiment in the new year

- Investors should consider buying Fortinet and Pinterest as the beaten-down growth stocks are poised to bounce back from 2022’s brutal selloff

- 2022 Performance: -32%

- Market Cap: $38.2 Billion

- 2022 Performance: -33.2%

- Market Cap: $15.5 Billion

Stocks on Wall Street have gotten off to a rough start in 2023 as worries over rising Fed rates, elevated inflation, and recessionary fears remained front and center for investors.

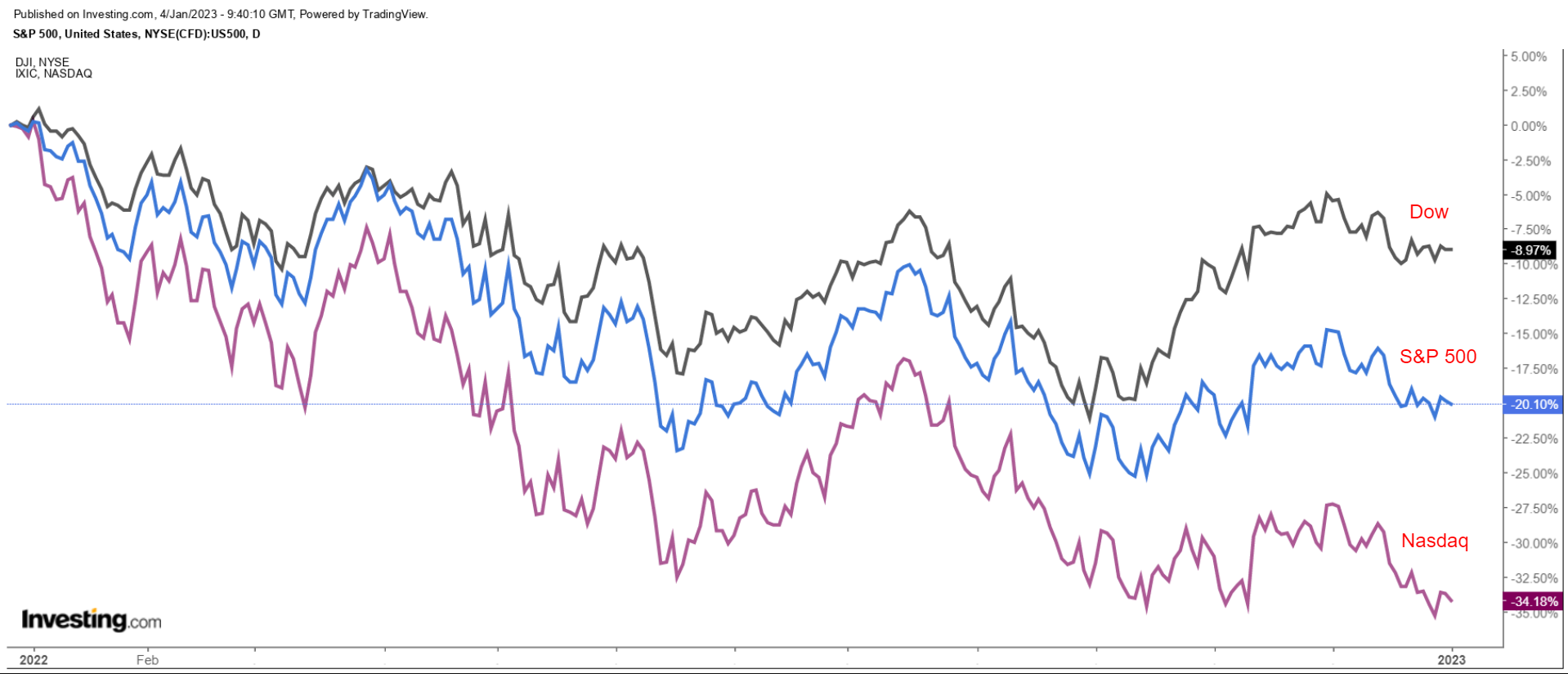

The major indices closed out 2022 with their worst annual declines since 2008. The blue-chip Dow Jones Industrial Average ended the year down 8.8% and 10.3% off its 52-week high. The benchmark S&P 500 lost 19.4% for the year and now sits more than 20% below its record high, while the tech-heavy Nasdaq Composite tumbled 33.1% last year.

With further volatility and market turmoil expected in 2023, I recommend buying shares of Fortinet (NASDAQ:FTNT) and Pinterest (NYSE:PINS) as the two beaten-down high-growth tech companies should offer solid upside given their improving fundamentals and reasonable valuations.

Fortinet

Widely considered one of the most prominent names in the cloud-based cybersecurity industry, I think Fortinet’s stock looks like a smart buy heading into 2023, especially at current valuations.

In my view, Fortinet, which develops and sells cybersecurity solutions, such as intrusion prevention systems and endpoint security components, is well-placed to reap the benefits of ongoing growth in cybersecurity spending due to the current geopolitical backdrop.

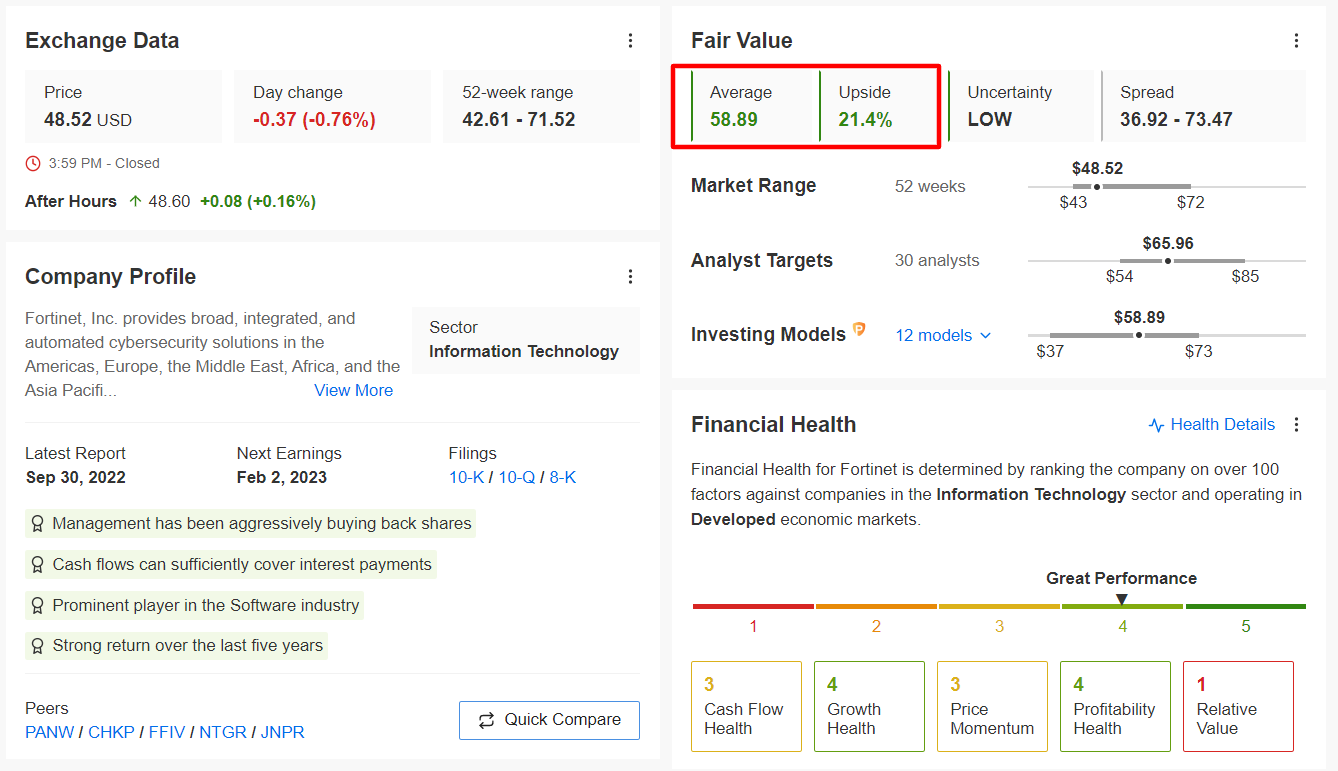

Indeed, 32 out of 33 analysts surveyed by Investing.com rate FTNT stock either as ‘buy’ or ‘neutral,’ reflecting a bullish recommendation. Among those surveyed, shares had roughly 36% upside potential based on Tuesday’s closing price.

Likewise, the quantitative models in InvestingPro point to a gain of 21.4% in Fortinet’s stock over the next 12 months, bringing shares closer to their fair value of $58.89.

The next major catalyst is expected to arrive next month when Fortinet reports fourth-quarter financial results after the U.S. market closes on Feb. 2.

Data from InvestingPro suggests that Wall Street analysts are extremely optimistic ahead of the report, with analysts raising their EPS estimates 27 times in the past 90 days to reflect an increase of 41.5% from their initial expectations.

Consensus calls for earnings per share of $0.39, compared to EPS of $1.23 in the year-ago period, while revenue is expected to climb roughly 35% year-over-year to $1.3 billion. If confirmed, that would mark the highest quarterly sales total in the company’s history, thanks to robust demand for its cloud-based security solutions from large enterprises.

Underlining the resilience of its business, the information-security firm has either matched or topped Wall Street’s profit and sales expectations for 19 straight quarters, dating back to Q4 2017.

FTNT - which slumped to a 52-week trough of $42.61 on Nov. 3 - closed at $48.52 yesterday, about 43% away from its all-time high of $74.35 touched in December 2021. At current levels, the Sunnyvale, California-based cybersecurity specialist has a market cap of $38.2 billion.

Shares of the network-security firm ended 2022 with a yearly loss of 32%, outpacing the annual performance of major industry peers, such as Crowdstrike (NASDAQ:CRWD) (-48.6%), Zscaler (NASDAQ:ZS) (-65.7%), and Okta (NASDAQ:OKTA) (-69.5%), while the Global X Cybersecurity ETF (NASDAQ:BUG) ended 2022 down 34.7%.

I believe Pinterest stock is set to recover from 2022’s brutal selloff and outperform in the year ahead as it remains well-positioned to achieve ongoing growth amid the challenging operating environment.

The San Francisco-based tech company stands to benefit from increasing budget allocations from advertisers thanks to its unique position in the social media, search, and shopping ecosystems. Despite worries over an industry-wide slowdown in digital advertising spending, Pinterest has seen companies flock to its platform as they seek to avoid the toxic and controversial content seen on other social media networks, such as Facebook (NASDAQ:META), Snap (NYSE:SNAP), Twitter and TikTok.

In addition, sentiment on the beaten-down name is likely to improve, given its positive fundamentals, stabilizing user growth, and increasing monetization potential under the continued leadership of CEO Bill Ready. The former Google (NASDAQ:GOOGL) e-commerce executive, who replaced founding CEO Ben Silbermann in June, has already made progress on the social media company’s turnaround efforts.

The company said in its Q3 earnings report, released in late-October:

“Despite the challenging macro environment, we are delivering performance and a distinct value proposition to advertisers, reaching users across the full funnel.

Through clear focus on increasing engagement that delights our users, we are deepening our monetization per user, and building personalized and relevant experiences that go from inspiration and intent to action.”

PINS - which fell to a 52-week low of $16.89 on May 24 - ended Tuesday’s session at $22.89. At current valuations, Pinterest, which is nearly 75% away from its all-time peak of $89.90, reached in February 2021, has a market cap of $15.5 billion.

Shares ended 2022 with an annual decline of 33.2%, easily outperforming Facebook-parent Meta Platforms’ stock, which sank 64.2%, and Snapchat-owner Snap, which saw its shares tumble 81%.

Wall Street has a long-term bullish view on PINS stock, with 33 out of 34 analysts surveyed by rating it as either ‘buy’ or ‘hold’. Shares have an average analyst price target of around $28.24, representing an upside of roughly 23% from current levels.

Similarly, the average fair value for Pinterest’s stock on according to a number of valuation models - including P/E multiples - implies a 19% upside over the next 12 months.

Disclosure: At the time of writing, Jesse is long on the S&P 500 and Nasdaq via the SPDR S&P 500 ETF (SPY (NYSE:SPY)) and Invesco QQQ ETF (QQQ). He is also long on the Technology Select Sector SPDR ETF (XLK) and the Energy Select Sector SPDR ETF (XLE).

The views discussed in this article are solely the opinion of the author and should not be taken as investment advice.

Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.